In 2025, US online gambling revenues reached $26.8 billion, a year‑on‑year increase of nearly 15 percent, driven by sports betting and iGaming growth in regulated states. Scale, profitability, and market positioning increasingly take precedence over expansion for operators. FanDuel, DraftKings, BetMGM, Caesars, and Fanatics are some of the major companies competing for market dominance.

The industry must strike a balance between expansion and tax demands, product development and regulatory control, and traditional land‑based models and digital‑first strategies. For the first time outside of the epidemic years, iGaming income in New Jersey exceeded traditional casino floors, marking a major change.

The US online gambling market generated $26.8 billion in revenue in 2025, a double‑digit growth over previous years. Sports betting was the main driver, with New York recording more than $2 billion in mobile revenue over the preceding 12 months. Over $1 billion was wagered annually on sports in Florida, Illinois, and New Jersey.

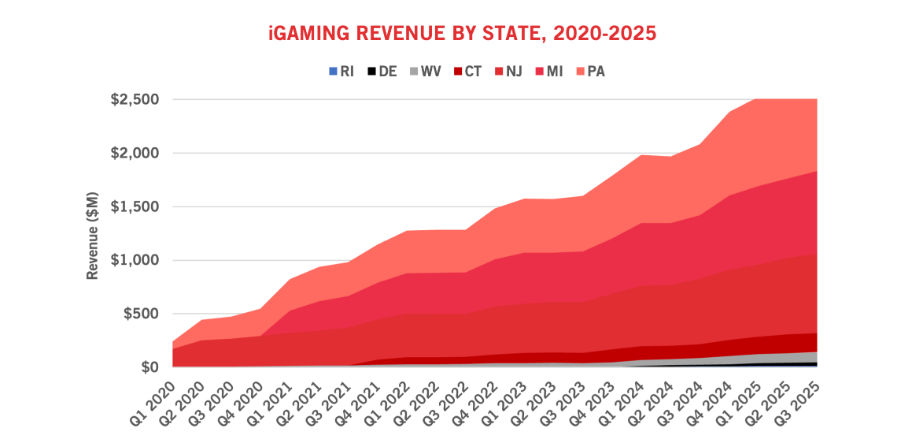

In seven states, New Jersey, Michigan, Pennsylvania, Connecticut, West Virginia, Delaware, and Rhode Island, iGaming reached all‑time highs. Revenues increased from $688.4 million to $907.4 million in October 2025. Pennsylvania had the highest gross gaming income last year ($3.3 billion), followed by Michigan ($2.9 billion) and New Jersey ($2.7 billion). In July 2025 alone, these states generated $877.3 million, a 28 percent rise over July 2024.

Operators placed greater emphasis on profitability, focusing on customer retention through loyalty programmes. Sports betting handle was estimated at $149 billion in 2024, underpinning the revenue growth seen in 2025. Projections suggest the market could exceed $41 billion in the coming years if expansion continues.

Gen Z accounted for 34 percent and millennials 42 percent of US betting activity in the second quarter of 2025, according to TransUnion’s US Betting Report. Overall, 30 percent of consumers engaged in betting during the period, up from 25 percent a year earlier. Land‑based casinos remained the most common choice, attracting 55 percent of bettors. Online casinos were used by 49 percent of respondents, online sportsbooks by 52 percent, and online lotteries by 41 percent. Land‑based venues also recorded increases, with sports betting rising to 43 percent and lottery participation to 45 percent. Millennials increased activity across most gambling categories, while Gen Z participation declined in several areas, except for online sports betting, which grew by 7 percent.

New Jersey reported $2.39 billion in annual iGaming revenue, with March 2025 contributing $243.9 million, a 23.7 percent increase from the previous year. Total gaming revenue for that month reached $546.1 million. With $673.3 million in revenue in the first quarter of 2025, iGaming generated $100.6 million in taxes and outpaced retail gaming by 4.5 percent. Although land‑based casinos topped that month with $265.3 million, May 2025 set a record at $246.8 million.

Michigan recorded monthly figures above $200 million, reaching $2.4 billion for the year. Pennsylvania reported $2.18 billion annually and $3.3 billion over the past 12 months, leading the US online casino market. All seven iGaming states posted record revenues in October 2025.

Sports betting also showed strong results. New York’s mobile market exceeded $2 billion in the past year, while Illinois and Florida each surpassed $1 billion in online sports betting revenue. In New Jersey, sports wagering handle reached $1.1 billion in March 2025, with year‑to‑date totals approaching $3.25 billion. These figures reflect concentrated growth in established markets as other states consider legalisation.

US iGaming revenue by state, 2020-2025 (Source: American Gaming Association)

iGaming revenue in New Jersey exceeded land‑based casino earnings in October 2024. While land‑based casino income decreased, iGaming revenue increased by 23.7 percent year‑on‑year to $243.9 million in March 2025. That month, iGaming paid $36.5 million in taxes to the state.

For the first quarter of 2025, iGaming revenue totalled $673.3 million, 4.5 percent higher than retail gaming. Sports betting handle approached $3.25 billion by March. In September 2025, annual iGaming revenue increased by 24 percent to $2.39 billion, nearly exceeding land‑based totals, while casino site income rose by 16.8 percent. New Jersey’s tax structure consistently maintained market success compared with states with higher tax rates, making it an important benchmark for iGaming activity.

In October 2025, total gaming revenue rose to $611.1 million, up more than 22 percent from a year earlier. Online gaming contributed most of the increase, with year‑to‑date revenue at $2.39 billion. State tax receipts reached $88.2 million in October and nearly $699.9 million for the year. The data shows online gaming has become a central part of New Jersey’s gambling market, consistently outpacing land‑based casinos. For operators, the results underline the need to protect market share in a mature iGaming environment through compliance and retention strategies.

The US sports betting market is consolidating, with FanDuel and DraftKings holding about 80 percent of the market share among the major operators. FanDuel reported revenue growth of around 29 percent to more than $7 billion in 2025, while DraftKings projected $6.3–$6.6 billion, a 39 percent increase year‑on‑year, aiming for its first full year of profitability with over six million monthly users.

In iGaming, BetMGM led with about a 22 percent share and expected $2.4–$2.5 billion in revenue. Caesars Digital projected $1.3–$1.5 billion and $500 million in EBITDA, supported by its rewards programme. Fanatics expanded its handle share to about 6 percent, projecting more than $2 billion in revenue, while BetRivers anticipated $1.0–$1.1 billion.

Operators face challenges, including higher taxes in states such as Ohio and Illinois, which put pressure on smaller firms. Payment restrictions from Visa and Mastercard have increased reliance on digital wallets and cryptocurrency, though fraud risks remain.

By 2029, iGaming is predicted to have grown from seven states in the United States to 10 to 15, with a projected total income of roughly $26 billion by 2030. Larger states would account for a considerable portion of this growth: if legalised, New York may contribute around 19 percent of revenues, while Ohio and Illinois combined might contribute 26–28 percent. The income source would be expanded beyond early adopters with authorisations in states such as Maryland, Louisiana, Colorado, and Wyoming.

Margin management is becoming increasingly common in operational strategies. In order to counteract increased tax rates, payment technology and artificial intelligence (AI) are being utilised to lower transaction costs, prevent fraud, automate risk management, and enhance client segmentation. The relevance of sweepstakes‑style products as alternatives to licensed iGaming is limited due to stricter regulations and legal concerns.

#USGaming #iGaming #SportsBetting #GamingRegulation #MarketTrends

Welcome to Gambling Consulting Authority (GCA) - Your Strategic Partner in Gambling Industry Advancement